The Death of the Interbank Market

The Death of the Interbank Market

a primer on the demise of Eurodollar and Fed Funds lending

After multiple significant crises, from a global pandemic to a subprime mortgage meltdown, the inner workings of the monetary system have changed forever. Monetary leaders have vowed to protect systemically important financial giants from collapse, implementing what Concoda calls The Big Three™: The Dodd-Frank Act (removing banks’ excessive risk-taking abilities), The Basel Framework (discouraging systemic risk and high levels of leverage), and the SEC’s money market reform (substituting riskier dollar funding sources with securer alternatives).

This assembly of rules and regulations has prompted Wall Street giants to withdraw from operating as major intermediaries and excessive speculators. Their role as risk-takers has been reassigned to the shadow banking layer, with securities dealers and other “shadow entities”, jargon for non-banks, absorbing banks’ now-prohibited operations.

As a result, a unique monetary paradigm has emerged. Banks no longer want to lend to each other, and even so, regulators won’t let them. Meanwhile, free from similar regulatory constraints, the shadow banking layer has proliferated, rising to over half the world’s assets. Secured dollar funding markets (like repo) have expanded, while unsecured markets (such as commercial paper) have halved in volume. The number of monetary transformations has kept ascending and shows no signs of stopping.

Perhaps the most unforeseen shift, however, has been the gradual demise of what was once the most crucial dollar funding market: the market for Federal Funds.

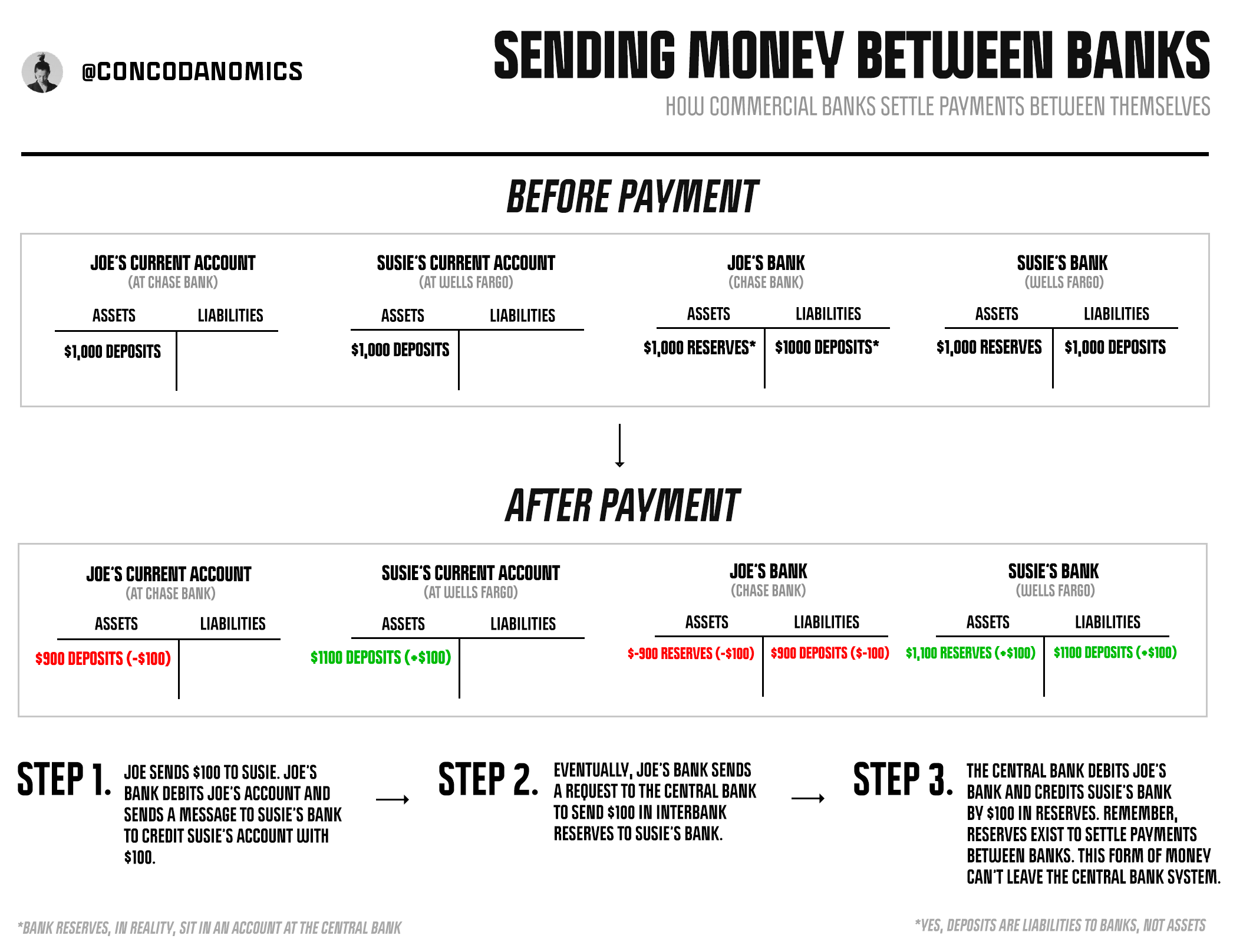

The Federal Funds (Fed Funds) market enables trading of Federal Reserve “settlement balances,” money created exclusively for entities under the U.S. government’s umbrella, primarily commercial banks but also government-sponsored enterprises (like Fannie Mae and Freddie Mac), thrifts, U.S. branches of foreign banks, and foreign official institutions. When U.S. and foreign citizens pay for goods and services in U.S. dollars, they use bank deposits created by commercial banks. Behind the scenes, though, the Federal Reserve System debits and credits the associated “Fed Master Accounts” — bank accounts issued to every entity with access to the Federal Reserve System — of every party involved in a transaction.

The rationale is to guarantee payment settlement among entities systemic to the global dollar banking system in all environments, but especially during financial crises. After decades of America’s private sector acting as an inadequate lender (and dealer) of last resort, the state has taken over the role of interbank (or “inter-Fed system”) payments. Subsequently, the banking system has become multi-layered: banks settle customer payments, and the central bank settles interbank payments.

Armed with state backing, Fed Funds — also known as “reserves”, “reserve balances”, “Deposits with F.R. Banks”, and the aforementioned “settlement balances” — are the most liquid form of U.S. dollars available. Even if an entity runs out of reserves to settle a payment, its local Federal Reserve bank will lend Fed Funds against high-quality collateral (usually U.S. Treasuries or agency securities). What’s more, reserves can also be converted into cold, hard physical banknotes, known officially as “vault cash”, by commercial banks to process customer ATM withdrawals. The Fed and its affiliates send an armored truck full of U.S. dollars to the bank’s requested branch, debiting its Fed Master Account as payment.

Trading of Fed Funds commenced in the 1920s, with only a few Federal Reserve member banks in New York City participating. A century of financial chaos and alchemy later, however, and the number of Fed Funds account holders had skyrocketed. Thousands of domestic and foreign financial institutions were joined by government sponsored-enterprises (GSEs) — Freddie Mac, Fannie Mae, Ginnie Mae, and the majority of Federal Home Loan Banks (FHLBs), plus many savings and loan associations.

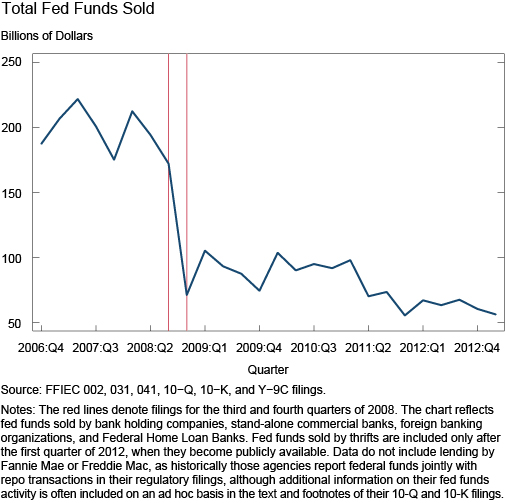

Up until the subprime meltdown, the Fed Funds market was flourishing. Volumes regularly exceeded $200 billion daily. On a typical day, often falling short of reserves, the Wall Street megabanks topped up their master accounts by borrowing excess Fed Funds from their smaller (usually regional bank) counterparts. But then the financial crisis changed everything, marking the beginning of the end of a bustling Fed Funds market. With the Big Three™ looming, interbank lending was doomed. The Fed Funds market — and along with it, the Eurodollar market — was about to transform.

{kind=link}