The Federal Reserve Endgame Is Not a Collapse, It's Global Domination

The Federal Reserve Endgame Is Not a Collapse, It's Global Domination

The longer America remains a lone superpower, the greater the Federal Reserve's reach over global finance

After a pandemic and multiple financial crises, we’ve finally entered a lengthy period of rising interest rates. But while most are aware of the ominous outcomes this could create, those who understand how the Fed actually controls interest rates will gain an edge in predicting the future.

Because of recent events ushering in exceptional circumstances, current textbooks describing how the Fed influences interest rates have become obsolete. Until recently, Federal Reserve officials could simply raise and lower interest rates by decreasing and increasing the level of bank reserves in the financial system. Bank reserves are “interbank” money, which can only be used by entities with reserve accounts inside the Federal Reserve System. JPMorgan, for instance, can pay Goldman Sachs for prime New York real estate using its reserves, while the average citizen must use bank deposits or “Federal Reserve Notes,” a fancy term for physical cash.

Before the Great Financial Crisis (GFC), the Federal Reserve had enough power to push interest rates toward its target, commonly known as the Federal Funds rate or EFFR — the price at which banks lend reserves to one another. The U.S central bank did so by adding and removing a specific amount of reserves to and from its interbank system. By lowering the supply of bank reserves, the Fed forced financial institutions to bid up the price of Federal Funds, resulting in higher interest rates throughout money markets. Conversely, by increasing the supply of bank reserves, the Fed influenced interest rates lower. The following graphic from the St. Louis Fed website illustrates these forces at work.

Everything ran smoothly. The Fed set a target range in which interest rates could fluctuate and made the necessary adjustments to keep rates within set boundaries. Conveying and implementing its latest monetary policy stance was a cakewalk.

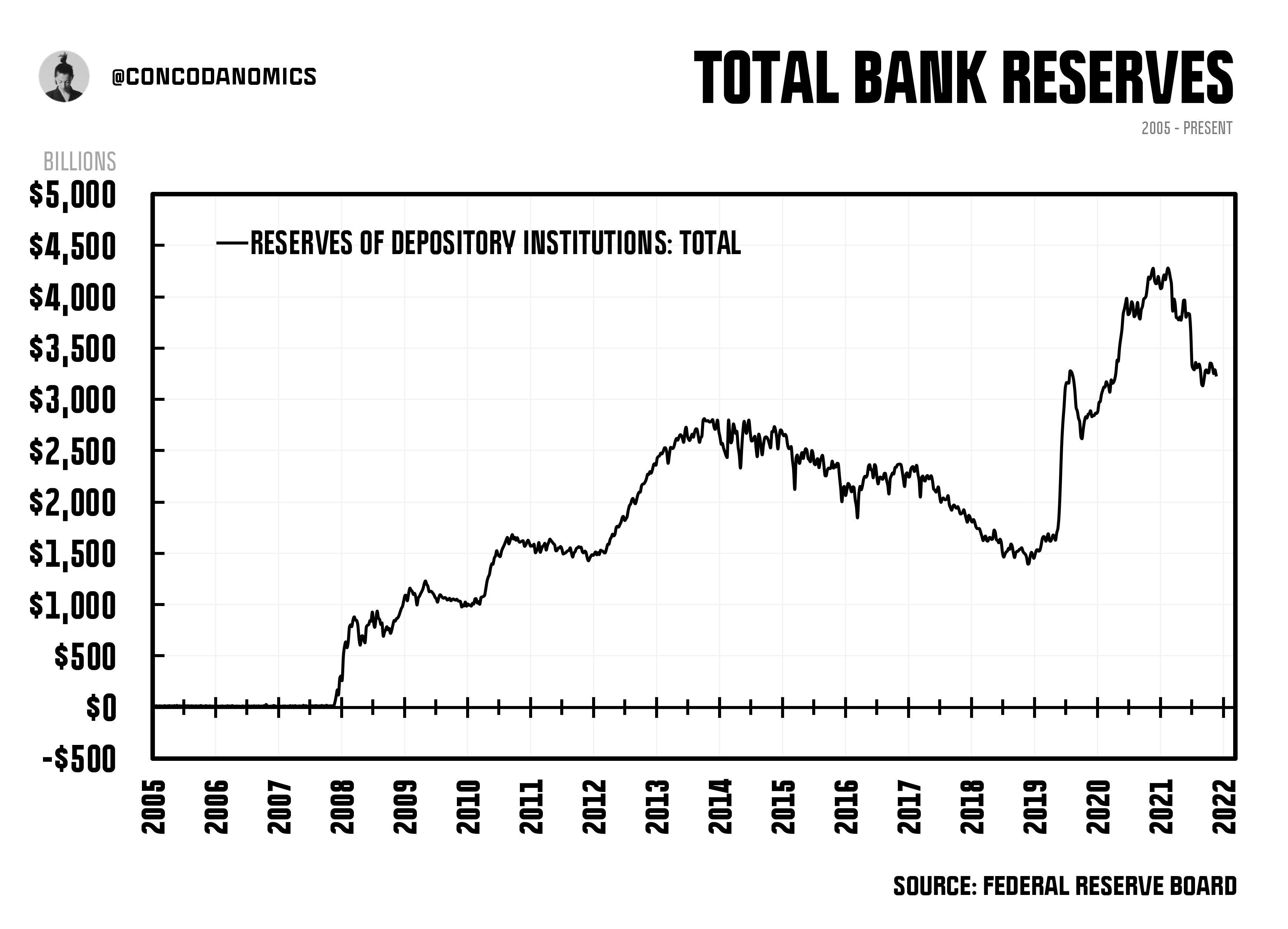

Then, in 2008, the Great Financial Crisis (GFC) hit, changing the central banking paradigm and the Federal Reserve System forever. The primary catalyst that fueled a radical transformation was the Fed officials’ decision to flood the system with bucketloads of reserves. The amount was staggering. In 2007, the system held a total of $15 billion in reserves. Today, that total has skyrocketed to roughly $3.2 trillion. The Fed’s latest quantitative tightening agenda has been aggressively eliminating bank reserves from the system. Still, it’s long before we return to “normal” levels.

With a system full to the brim with reserves, the Fed could no longer control interest rates through its previous policy of increasing and decreasing levels of interbank money. As shown in the graphic below, the Fed flooding the system with reserves meant that even sizeable supply adjustments no longer influenced the demand curve. The U.S central bank needed a new mechanism to take back control of Federal Funds and fast.

Enter the Fed’s “Ample Reserves” regime, where Fed officials stopped using open market operations (OMOs) — buying and selling government securities to alter reserve levels — as its primary tool to adjust the price of money. On October 6th, 2008, the Fed began paying reserve account holders, mostly large commercial banks and government-sponsored enterprises (GSEs), interest on their balances. IOER (Interest On Excess Reserves), as it was called back then, had been chosen as the Fed’s chief tool to control interest rates.

By offering banks IOER, a “risk-free” investment option, the Fed gained the power to control money markets through two mechanisms. First, through the “reservation rate,” the lowest rate that banks were willing to loan out funds to the market. Because the Fed started handing out a risk-free investment that paid superior interest (IOER), no entity would want to lend to others at rates lower than the Fed. This set a ceiling on how high rates could go, alongside the Fed’s second mechanism: arbitrage. Fed Funds rarely dropped beneath IOER because entities could create a risk-free arbitrage, borrowing Fed Funds at say 1% and depositing it at the Fed, which paid out 1.5%. The 50 basis points gap would eventually narrow to near zero, as Fed Funds participants competed to arbitrage the spread away.

With these two new levers, the Fed believed it had successfully regained control of money markets. If it wanted to alter rates, the Fed simply adjusted the discount rate and IOER at the same time and by the same level. If the FOMC (Federal Open Market Committee) was indicating that rates should rise, money markets could adjust, preemptively pricing in a tightening cycle.